Flatbed & Truckload Market Outlook

March 2026

The U.S. truckload market is beginning to show early signs of tightening after nearly three years of freight recession. Capacity reductions, improving industrial demand, and rising diesel prices are all contributing to a gradual shift in market conditions.

Flatbed freight in particular is starting to show momentum. Because flatbed equipment is closely tied to construction, manufacturing, and infrastructure activity, it often provides the earliest signals of broader changes across the truckload market.

Below is a look at the key forces shaping the market today.

TL;DR — Market Snapshot

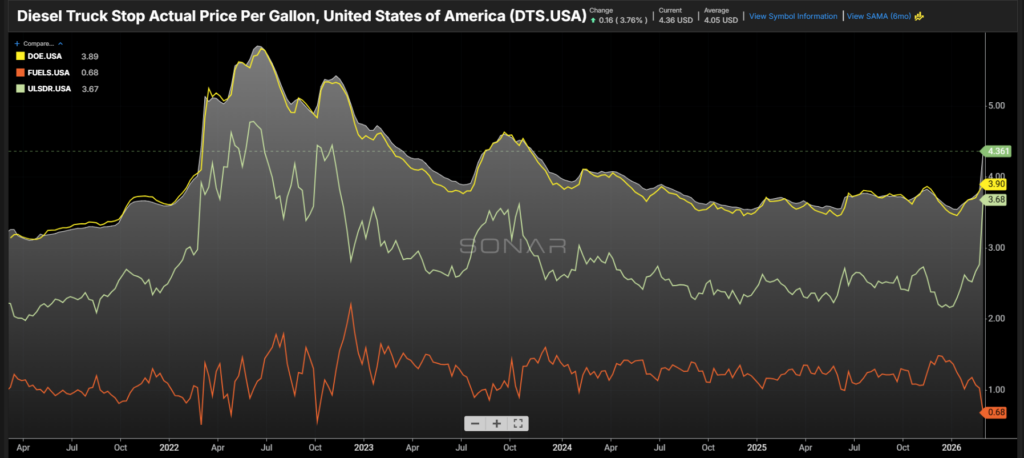

Fuel

- Diesel prices have climbed steadily to start the year, reaching roughly $3.90 per gallon nationally in early March.

- Prices have increased roughly $0.20 over the past month, driven by higher crude prices and geopolitical uncertainty.

- Rising fuel costs increase trucking operating expenses and push fuel surcharges higher across the industry.

Flatbed Demand

- Flatbed demand has improved sequentially to begin 2026, though it still remains slightly below historical seasonal strength.

- Early demand growth is coming from industrial freight, infrastructure projects, and construction activity beginning to ramp up ahead of spring.

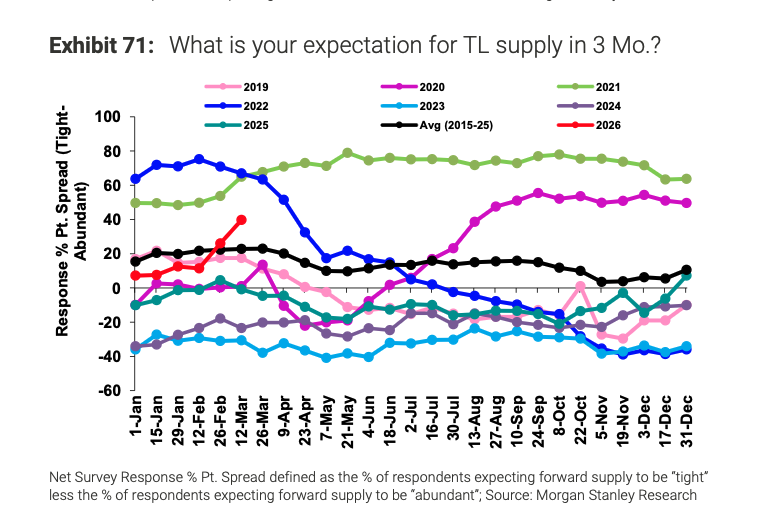

Capacity

- Truckload capacity continues to tighten as carriers exit the market following a prolonged freight downturn.

- Additional pressures on supply include:

- regulatory enforcement

- driver availability

- weather disruptions

- reduced tolerance for unprofitable lanes

Rates

- Spot rates have stabilized after an extended decline and are beginning to trend upward.

- Early contract bid cycles are already showing upward pressure on pricing for 2026.

Bottom Line

The freight downturn appears to be approaching the end of its cycle. Tightening capacity and improving demand suggest gradual upward pressure on rates throughout the remainder of the year.

Industry Commentary

Market sentiment is shifting as capacity tightens and freight demand slowly improves.

Below are several perspectives from across the industry.

Carrier Perspective

“Capacity appears to be tight across both open deck and van sectors. We are starting to see stronger demand in the industrial and construction sectors.”

— Carrier

“The demand and rates are in our favor — and this is before construction season starts.”

— Carrier

“Capacity has tightened greatly. Our trucks are going to the direct shippers that have been with us over the last three years and are benefiting from their loyalty.”

— Carrier

Shipper Perspective

“Entering the 2026 bid season, we are seeing carriers request relief on contracted lanes that no longer fit their networks. We expect steeper increases on lanes without strong backhaul or volume density.”

— Shipper

“Just when networks were starting to stabilize, weather disruptions hit again. There are opportunities for carriers to take increases this year.”

— Shipper

Broker Perspective

“Spot rates in most major outbound markets are up anywhere from 15% to 30% since early January depending on equipment and market.”

— Broker

“There has been a lot of commentary about supply leaving the market driving spot rates up, but there is still limited hard data explaining exactly why supply has exited.”

— Broker

Overall Sentiment

Across carriers, brokers, and shippers, the consensus is that capacity is tightening and pricing power is gradually shifting back toward carriers, although some uncertainty remains around the pace of demand recovery.

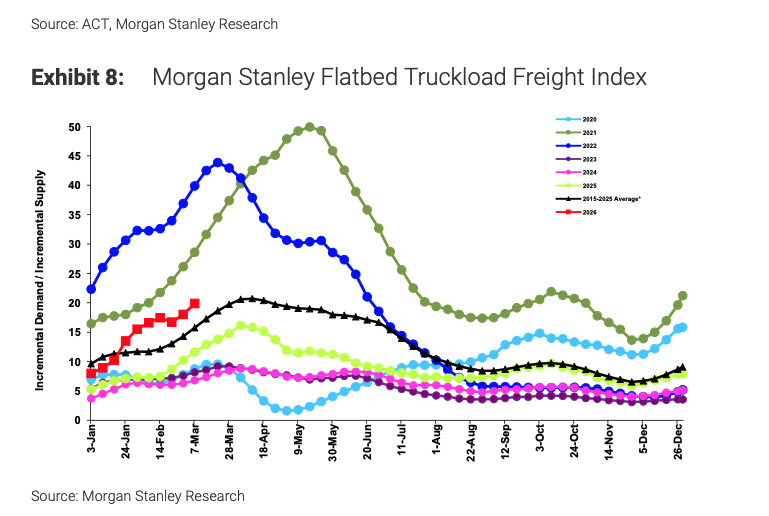

Flatbed Market Indicators

Flatbed freight activity is one of the earliest indicators of broader truckload market shifts because it closely follows activity in:

- construction

- manufacturing

- infrastructure

- energy development

Recent data shows the flatbed freight index trending upward in early 2026, indicating improving demand relative to available truck capacity.

While the market remains well below the peak conditions seen during the 2021 freight boom, the recent upward movement suggests the industry may be entering the early stage of a tightening cycle.

This shift is being driven by several key factors:

• increased industrial activity

• early construction demand ahead of spring projects

• continued carrier exits after the freight downturn

• regulatory enforcement affecting available capacity

Flatbed markets often move first in freight cycles. If current trends continue, broader truckload markets may follow later in the year.

Flatbed Rate Trends

Flatbed spot rates remain well below the highs reached during the 2021–2022 freight boom. However, pricing has stabilized and begun to trend higher in several key markets.

Contract pricing has remained more stable than spot pricing during the downturn, but early bid activity suggests moderate increases may be ahead in 2026, particularly in lanes where:

- backhaul options are limited

- project freight demand is increasing

- construction and infrastructure activity is concentrated

What This Means for Shippers

For companies moving heavy freight, construction materials, or project cargo, the market environment may begin to change throughout the year.

Several trends are worth watching:

• Flatbed capacity may tighten through Q2 and Q3

• Project freight lead times may increase

• Flatbed spot pricing could gradually rise

• Strategic carrier relationships will become increasingly important

Companies involved in infrastructure, energy, and industrial construction may benefit from planning transportation capacity earlier in project timelines as the market continues to tighten.

Looking Ahead

While the recovery remains gradual, many signals suggest the freight market is beginning to transition out of its prolonged downturn.

Flatbed markets are already showing early strength, and if industrial demand continues to improve through the spring and summer, the broader truckload market may follow.

CargoVolt will continue monitoring these trends and sharing regular updates as the market evolves.

CargoVolt

Specialized Logistics for Energy, Infrastructure, and Industrial Freight